Your cart is currently empty!

RKT-COOP

Only Upside Potential for Rocket Companies (RKT): Lower Rates, Higher Mortgage Volume, and Revenue Diversification

Key Highlights

- When interest rates were at a peak, I found out about Mr. Cooper Group, Inc.- the stock was trading at $42. It’s been breaking all time highs ever since. Now Rocket Companies, Inc. comes around the corner with a bold stock deal.

- RKT is expending its recurring revenue servicing portfolio by a staggering $900B+, giving it a combined servicing power of over $1 trillion.

- RKT is diversifying its revenue stream right before interest rates are lowering significantly – a smart move.

- RKT’s moat from its brand and tech platform is being deepened by the new servicing branch of COOP.

- RKT stock keeps outperforming COOP, giving COOP more and more upside potential in stock price. I hold positions in both and, even though I placed stoploss levels, I am not worried about downside potential.

My Introduction to Mr. Cooper

I first discovered Mr. Cooper (COOP) during the 2022–2023 cycle of interest rate hikes. While most mortgage lenders struggled, Mr. Cooper stood out. At the time, COOP was trading around $42 per share, and it seemed to thrive in an environment that should have crushed its margins. That was my first clue: this company was built differently.

Since then, COOP has done nothing but break all-time high after all-time high, showcasing strong execution, growing profitability, and a countercyclical edge due to its massive servicing portfolio. It quickly became one of the most impressive compounders in the financial sector—quiet, efficient, and resilient.

So when Rocket Companies announced its plan to acquire Mr. Cooper in 2025, my first reaction was: this could be a power move.

A Snapshot of Rocket’s Ecosystem

Based in Detroit, Rocket Companies is more than just a mortgage lender—it’s a vertically integrated fintech platform. Its ecosystem includes:

- Rocket Mortgage – the largest retail mortgage lender in the U.S.

- Rocket Homes – a real estate search and agent referral platform.

- Rocket Auto – an end-to-end vehicle buying and financing platform.

- Rocket Loans – offering personal loans via a digital-first experience.

- Rocket Money – a personal finance app that helps users manage subscriptions and track spending.

- Canadian expansions through Lendesk and Edison Financial.

What ties these all together? A proprietary technology platform designed to simplify and digitize financial decisions—whether it’s buying a home, a car, or consolidating debt.

Why the Mr. Cooper Acquisition Matters

In fall 2025, Rocket plans to close its acquisition of Mr. Cooper Group Inc. (COOP) in a stock-for-stock deal valued around $9.2 billion. This isn’t just another merger—this is a game-changer.

Here’s what it unlocks:

🔁 Revenue Diversification

Rocket’s primary income stream—mortgage origination—is notoriously cyclical and sensitive to interest rates. Mr. Cooper, however, brings a massive $900+ billion servicing portfolio to the table. This will create recurring, stable revenue and reduce Rocket’s earnings volatility in volatile rate environments.

🚀 Scale and Leadership

The combined company will manage over $1 trillion in servicing volume, making it one of the largest mortgage servicers in the U.S. This scale brings serious competitive advantages, from operational efficiency to better pricing power.

💡 Technology Synergies

Mr. Cooper’s servicing platform will be integrated into Rocket’s digital ecosystem, which could massively improve:

- Customer retention

- Cross-selling opportunities (e.g., insurance, equity loans, budgeting tools)

- End-to-end customer lifetime value

Tailwinds in 2025 and Beyond

Several macroeconomic factors are lining up in Rocket’s favor:

✅ Falling interest rates: Expected Fed rate cuts should increase mortgage demand.

✅ Refinance resurgence: A decline in rates will revive refinancing, which has been dormant since 2022.

✅ Tech-driven margins: Rocket’s platform allows it to scale without a corresponding rise in costs.

✅ Strong leadership: CEO Varun Krishna (ex-Intuit, PayPal) is doubling down on product innovation and long-term platform value.

New Mortgage Applications and Existing Mortgage Refinances

What About COOP Shareholders?

If you currently hold Mr. Cooper shares, here’s what to expect:

- You’ll receive Rocket shares based on a fixed exchange ratio once the deal closes. The terms of agreement showed a 1:11 ratio of COOP to RKT shares.

- You’ll be part of a larger, more diversified company with both origination and servicing revenue streams.

- If Rocket’s stock performs well post-merger, you stand to gain significantly from long-term upside.

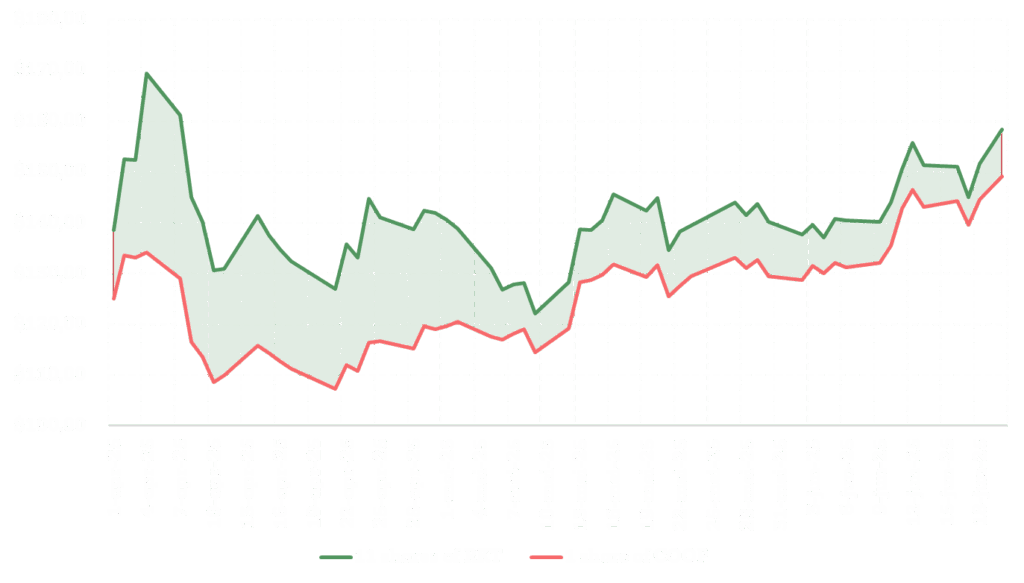

What does the 1:11 stock ratio mean?

RKT is said to takeover COOP by a stock ratio of 1:11. This means, that for every COOP share you hold, you will receive 11 RKT shares. Reason enough to track the performance of both stocks and how the price of a COOP share corresponds to 11 shares of RKT, as you can see in the graph above. The graph clearly shows that RKT keeps outperforming COOP and as of now, the 1:11 ratio gives COOP another 6.22% upside potential.

- Share price of RKT: $14.40 as of last close friday June 20th

- Share price of COOP: $149.12 as of last close friday June 20th

- Price of 11 shares of RKT: $14.40 * 11 = $158.40 – giving COOP 6.22% room to grow from $149.12

Comments