Your cart is currently empty!

Landing gear

Did the FED forget its landing gear?

More than three years ago, the Federal Reserve started discussing quantitative tightening and raising interest rates. The result? A short bear market, with the S&P 500 dropping over 25%, and panic spreading through the media. In the meantime, all financial markets have reached new all-time highs, and everyone keeps talking about a soft landing. Is it still possible, or did the FED forget to deploy its landing gear?

Who doesn’t like wage growth?

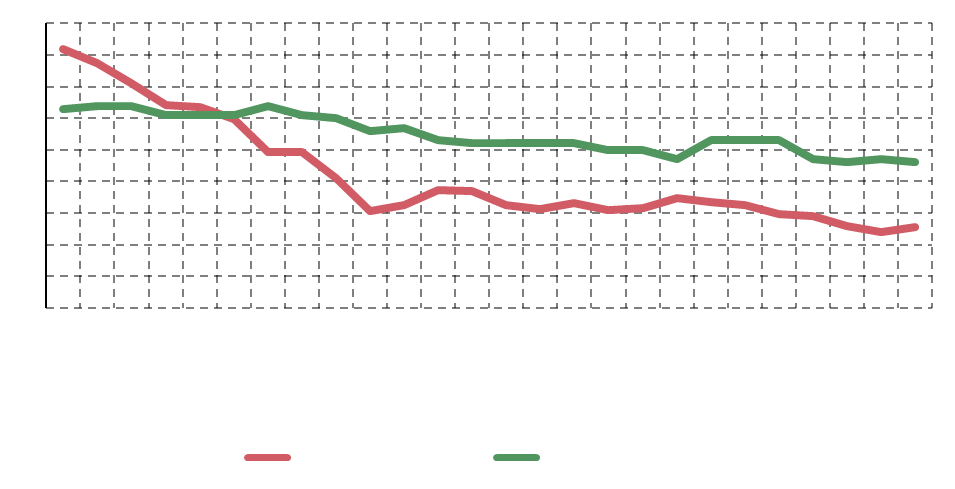

During times of inflation, all I hear are complaints about expensive groceries and demands for higher wages. Everyone wants their wages to rise alongside inflation. In a sense, it’s a logical reaction—no one wants their money’s value to evaporate without compensation. However, if wages keep rising alongside inflation, we could end up in a dangerous price-wage spiral. This occurs when wages rise in response to rising prices, perpetuating the cycle.

Interestingly, headline inflation in the U.S. dropped below wage growth in February 2023 and has remained that way since. For nearly two years, wage growth has outpaced inflation. This, as I noted earlier, coincides with the improvement in consumer sentiment in January 2023. However, people need to consider the bigger picture. Wage growth has been steadily declining, and since June 2023, real disposable income growth has followed suit.

Labour market or inflation?

To achieve a soft landing, the FED will likely start cutting interest rates gradually. Meanwhile, it is monitoring the labour market more closely than its preferred inflation measure, the Personal Consumption Expenditure (PCE) index. The aggressive interest rate hikes didn’t harm the labour market as severely as many had feared when the tightening cycle began. This resilience fuels the hope for a soft landing.

However, many people assess the labour market primarily through the Non-Farm Payroll (NFP) numbers. With a new government taking office next month, attention should also turn to the plans of the new Department of Government Efficiency. One key initiative involves reducing government jobs, which have accounted for an average of around 41,000 new jobs per month over the past two years. While the unemployment rate is already showing upward momentum, laying off federal workers could exacerbate this trend. Moreover, it’s not just federal jobs at risk—since the labour market’s recovery from the COVID-19 crash, the number of overall layoffs and discharges has been steadily increasing.

So what is the FED facing?

Wage growth remains significantly above inflation. Future job creation is uncertain. Unemployment is showing upward momentum. To support the labour market, the FED might consider further interest rate cuts. However, lower interest rates could encourage more borrowing and spending, which, in turn, might drive inflation higher. If that happens, the FED might need to counter inflation again by increasing interest rates to curb borrowing and spending. This cycle could further destabilize the labour market, making a hard landing more likely.

While initiating the landing, did the FED forget its landing gear?

Comments